Money and Mental Health: Financial Therapy Explained

May is Mental Health Awareness Month, and this year I want to talk about something that still doesn't get enough attention: the connection between money and mental health.

I've worked with clients as young as 8 and as old as 78. What I've seen across every age, every background, every income level is this: our relationship with money is deeply personal, deeply emotional, and often deeply inherited. As Dr. Wallace wrote in Generational Wealth Begins with Generational Knowledge, the way we feel about money is a greater indicator of financial health than the amount of money in our bank account.

Your Relationship with Money Started Before You Did

Most people don't realize that their financial behaviors were shaped long before they earned their first dollar. The way your parents and grandparents talked about money… or more commonly, they didn't strongly impacted the reality of your financial state today.

I've sat with clients in their 70s who still hear their father's voice when they check their bank account. I've worked with children whose anxiety about money was absorbing stress they couldn't even name yet. This is what I mean by the generational effects of money and mental health. It doesn't start with you, and if you don't address it, it doesn't end with you either.

Financial therapy exists to bridge the gap between mental health and money management.

From Age 8 to 78: What Generational Money Stress Looks Like

When I work with a child who's anxious about money, I almost always find an adult in their life who's anxious about money too. The child didn't learn this from a textbook. They learned it from the dinner table, the car ride home from the store, the tension in their parent's voices when a bill arrived.

When I work with someone in their 60s or 70s who can't stop working even though they have enough, I almost always find a story about poverty, loss, or instability somewhere in their history whether it's from their own childhood, or their parents', or their grandparents'.

The 8-year-old who hoards birthday money because they sense their family's financial stress. The 78-year-old who still panics about spending because they grew up during a time when there was never enough. The college student drowning in impulsive spending and credit card debt because no one ever modeled a healthy relationship with money for them. The middle-aged professional burning out because they tied their entire self-worth to their income.

Same root. Different branches. This is what makes money and mental health inseparable. Financial behavior isn't rational. It's inherited, adapted, reinforced, and often passed down without a single word being spoken about it.

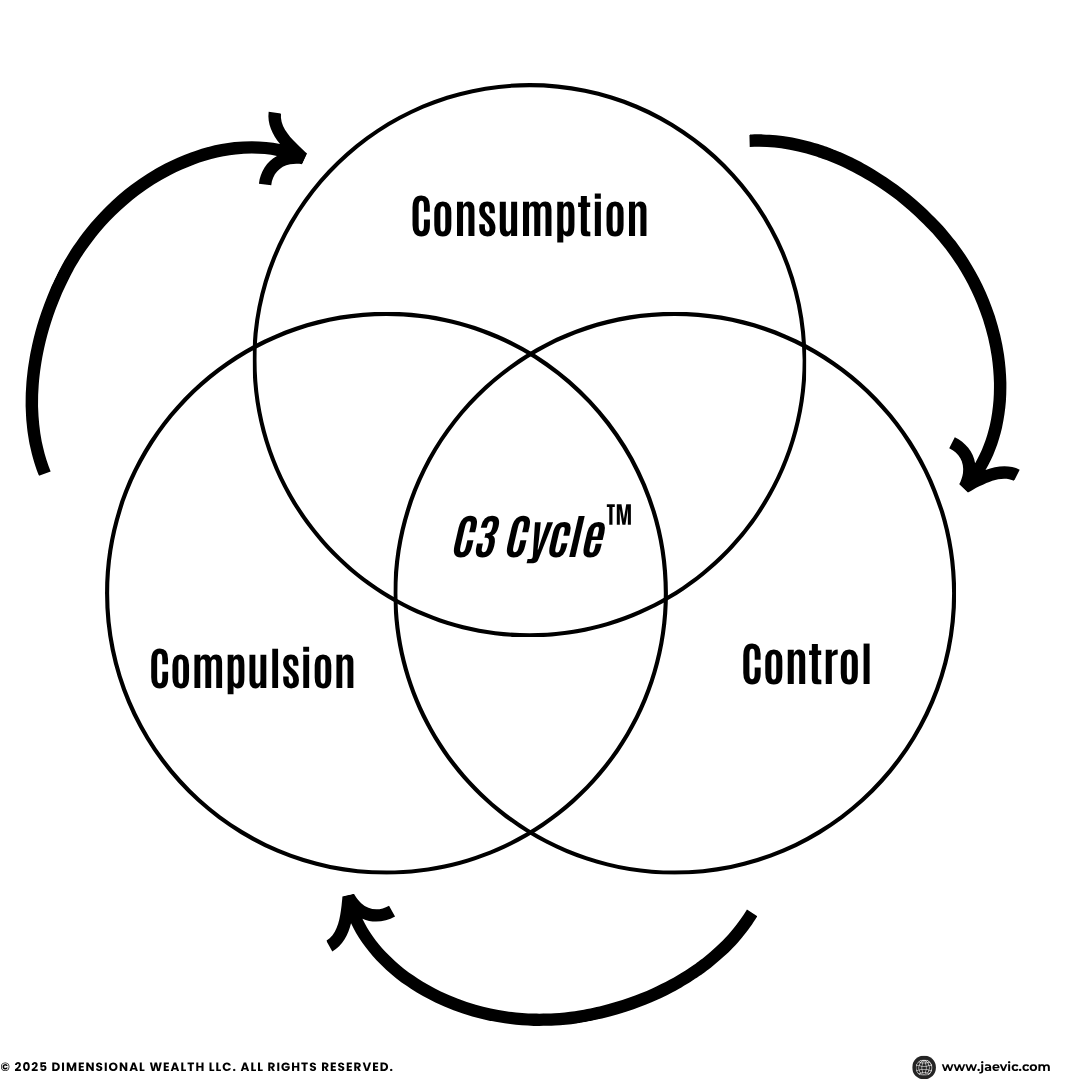

The C3 Cycle™ — Jaelyn Vickery, CFT’s trademarked consumer psychology framework for understanding impulsive spending, emotional consumption, and behavioral money patterns.

What Happens After You Hit "Purchase"

One of the patterns I see most often across all ages, incomes, and backgrounds is the cycle of impulsive spending.

I call it the C3 Cycle™: Compulsion, Consumption, Control.

Compulsion — something triggers the urge. Stress, boredom, shame, a bad day, a good day you feel guilty about, seeing something that reminds you of what you don't have.

Consumption — the impulsive behavior via purchase happens. Food, clothes, electronics, subscriptions, a cart full of things you didn't plan to buy. In the moment, it feels like relief. Like you're doing something for yourself. Like you deserve this.

Control — then the reality sets in. The guilt. The shame. The overdraft notification. The "Why did I do that again?" spiral. And often, the attempt to overcompensate through restriction, avoidance, or doubling down on a budget your cycles will cause you to break within a week.

This cycle lives at the intersection of consumer psychology and emotional well-being. The distress that follows impulsive spending isn't just about the money you spent. The answer to end destructive impulsive spending cycles is to understand the relationship you have with yourself around money. The shame and guilt is information financial therapists utilize as an asset of understanding. Most financial advisors skip right past those feelings and go straight to "make a budget." Then clients wonder why they can’t sustain change in their money habits. That's like telling someone with disordered eating to just meal prep.

Food, Finance, and Retail: The Same Pattern, Different Aisles

One of the most important things I've learned across my caseload is that impulsive spending rarely shows up in isolation. The same patterns that drive financial distress often show up in how people relate to food, shopping, and consumption more broadly.

A client who stress-spends at Target is often the same client who stress-eats after a long day. A client who avoids looking at their bank account is often the same client who avoids stepping on the scale. These aren't separate problems. They're the same problem expressing itself in different ways.

This is what I mean when I talk about Disordered Consumption™. A pattern of using consumption to manage emotions that don't have anything to do with what you're buying or eating. It carries a particular kind of shame, because our culture tells you overconsumption is your fault. You should have more self-control. You should be better with money. You should be smarter about this by now. Financial therapy at Dimensional Wealth challenges that story by understanding what drives the behavior.

What Financial Therapy Actually Looks Like

This is the part most people can't picture. So let me walk you through it.

Financial therapy isn't someone reading your bank statements back to you or telling you to not spend money. It isn't a financial advisor overselling products to you for commission. And it isn't just therapy that happens to mention money. Financial therapy is a specialized approach that combines therapeutic techniques with financial knowledge to help you change your relationship with money at the root, not just at the surface.

In a session, that might look like:

Unpacking a spending episode: not to judge it, but to understand what triggered it, what feeling you were chasing, and what happened after. We slow down the C3 Cycle™ and look at it together.

Exploring money stories: where did your beliefs about money come from? What did your family model? What messages did you absorb about wealth, spending, saving, and your own worth before you had any say in it?

Building financial self-trust: not through willpower, but through understanding your patterns, developing awareness of your triggers, and creating systems that work with your psychology instead of against it.

Addressing the emotions that budgets can't fix: shame, guilt, fear, perfectionism, comparison, grief, generational trauma. These are the real barriers to financial wellness, and no spreadsheet addresses them.

A session might last 30 minutes or 90 minutes. You might come every week or every other week. There's no fixed formula, because every person's relationship with money is different.

What is consistent is this: we're not working on your money. We're working on you. The money changes when you do. At Dimensional Wealth, you become the architect of your wealth.

Why This Matters Right Now

May is Mental Health Awareness Month, and every year the conversation gets broader about what mental health actually includes. Anxiety. Depression. Trauma. Relationships. Body image.

But money is still treated like a separate category. Money management is pain management. Money stress impacts our mental health. Financial overwhelm affects your sleep, your relationships, your body, your self-worth. The shame around financial struggles keeps people from getting help because we've been taught that money problems are personal failures, not health concerns.

If you want to create lasting financial change in your life, here are three starting points:

1. Name the pattern. Not to judge it, but to see it. Are you in a C3 Cycle™? Are you stress-spending, stress-eating, or stress-avoiding? Awareness is always the beginning.

2. Ask where it started. What did money mean in your family? What did you learn about spending, saving, and your own worth before you had any say in it?

3. Talk to someone who gets it. Financial therapy is specifically designed for this intersection. Not therapy that sometimes mentions money. Not financial advice that ignores emotions. The actual space where both meet.

If you're in Champaign, Illinois or anywhere in the United States, Dimensional Wealth provides services in-person and virtually. You can book a free consultation to see if financial therapy or money coaching is the right next step for you.

Jaelyn Vickery, CFT, is the founder of Dimensional Wealth LLC and host of the Finance, Fitness & Finesse (F3) podcast. She specializes in impulsive spending, financial therapy, money coaching, and helping people build wealth with wellness — in Champaign, IL and virtually nationwide.